Assault #5 on Main Street retailers

Covid-19 is the latest assault on the livelihood of “Main Street” (as opposed to Wall/Bay Street/Madison Avenue) retailers and local businesses. Main Street retailers, for me anyhow, are typically small and medium sized business as family operations meet the needs and aspirations of their local communities. They are oftentimes the element that makes living in any particular neighbourhood or community richer, and they are a vital contributor to the local business ecosystem. Pretty much all the sponsors of kids’ sports teams I played on – hockey, baseball, flag football, football – were local small businesses. Not a Wall/Bay Street sponsor to be seen anywhere.

I happen to live and work and play in a “15-minute neighbourhood”, one of those urban communities, in which there is a full and vital array of places to live, work, play and shop that are all within at most a 15-minute bike ride or about a 20-minute walk. I am concerned that Covid-19 may be the assault on Main Street businesses that finally breaks the will and the resilience of these local institutions. This last assault may prove to be just too much for them to survive or commit to attempt recovery.

typical Main Street retail my neighbourhood

Assault #1: Walmart in the 1990s

Walmart started in small town North America and offered much of what was sold by smaller firms located on the main drag at prices Main Street retailers could not match. If I have it right, every Walmart local manager had pricing leeway on the top 100 selling items to beat out the local competition.

Walmart was an innovator in supply chain management as well. It made better use of its scale and strength with suppliers to improve the efficiency of its inventory and stock. It could demand terms from suppliers that no Main Street retailer could match. And it passed some of those savings onto customers.

Assault #2: Power centers, big box stores and category killers in the 1990s

Funny thing, other retailers noticed the success of Walmart and developed new stores like Costco, Price Club, Home Depot and Lowe’s that were massive – big boxes – in size. That scale allowed them to provide significantly more stock, making themselves the place to go to get all your needs met. They had pricing power with suppliers as they grew, and they worked to sell inventory in days that they would pay for in weeks.

The category killers would specialize within a retail category and overwhelm the competition in scale, selection and price. Think Barnes and Noble for books, Staples for office supplies, Best Buy for home electronics, or Toys R Us at Christmas.

The formula for a power centre was get a very large site to accommodate a big box retailer, surround it with category killers, put in some pads for chain restaurants and have plenty of parking. That sort of large land mass was usually only available out in the suburbs and well away from Main Street.

representative power center site

Main Street businesses were under pressure to compete on price or make sell items not available from big boxes or category killers, and hope that their convenience and customer service experience would win out.

Assault #3: Amazon in the 2000s

Amazon did something really cool when they started – they made it easy for me to get books that just weren’t available in my market. While where I live is not small (Ottawa had a CMA population of about 1.0 million then), there are many items I was interested in that could only be found in the stores in much bigger markets. Now the playing field was a little more even as I could buy those hard-to-source locally items. Yes, I could go to my local bookstore and have them order it, only Amazon delivered it faster and the website also had reviews of the book and could point to other similar books that could be of interest.

The challenge for my local bookstore is that Amazon had collected the buying habits of many more customers and that allowed them to make other recommendations for what could be of interest. Amazon was collecting and exploiting the big data flowing from all those searches and purchases by all those customers. My “search for the right book” experience as opposed to my “buying experience” was richer as a result. My local book seller needed to up its game, make that “buying experience” richer somehow or specialize in a narrower range of books.

I really enjoyed the bookstore in Chicago that had a grand piano as well as sheet music. It was no where near as nice as this one in Buenos Aires. Why is it that Latin American countries still have great bookstores?

Assault #4: Ecommerce goes from laptop to phone apps in the 2010s

More retailers make it easier for customers to order goods from their phone. Delivery times improve. The assault on Main Street is two-fold: convenience and selection. It is pretty convenient to do any shopping from your phone and get quick home delivery.

The likes of Etsy and Shopify help the Main Street retailer compete with e-commerce, but the strength and breadth of mammoth e-commerce firms is making it increasingly difficult for the Small to Medium Enterprises (SME) to compete.

Assault #5: Covid-19 in the 2020s

Tobias Lutke, the CEO of Shopify, said that in the 4 months of Covid-19, they accelerated their business to levels expected by 2030, and not mid-2020. E-commerce generally is greatly expanded, and work from home or remote working is likely to reinforce e-commerce as opposed to dilute its effects as we adjust to life with Covid-19. The following chart using UK data shows the spike in e-commerce sales in the UK.

Financial Times: A Nation of Shopkeepers shaken by the shift online

Some of the bars, restaurants, local boutiques and local businesses that rely on the foot traffic of my 15-minute neighbourhood may not survive. There will be an increasing number of papered up storefronts leading to cash flow issues for landlords, and problem loans for banks.

The Phoenix rising from the ashes

I often wonder what leads to that new funky neighbourhood filled with local boutiques, art houses, and local cafes, bars and restaurants. I suspect that transformation is lead by the decline and gentrification of real estate past its prime and overtaken by other locations. The decline hits the neighbourhood, it gets to be inexpensive and that is when the new breed of local retailers arrive to exploit inexpensive rents.

Covid-19 will be driving the business failures and bankruptcies that eventually generate new retailers. That creative destruction takes a while to complete.

All these assaults are having an impact on the tenets of retailers. These include:

Big Data Dominance

My Main Street business does not have access to the big data collected by apps and e-commerce firms.

I worked with Canadian Tire doing site selection in the mid-1990s. One of its sources of data then was credit card intel from those of its clientele that paid with their Canadian Tire credit card. That gave them access to information about spending habits and stores frequented that was unavailable to other retailers. This data is rudimentary to that tracked and collected now by Google, Amazon, Facebook and the like.

Location: is the anchor model dead?

The mantra in real estate has been “location, location, location”. What that meant for site selection for retailers had been to figure out a part of town that did not have what you sell, figure out how big that trade area is and how much disposable income it represents, make an estimate for potential sales, and then figure out if you co-locate close to a retailer with an even bigger draw of potential customers – an anchor – maybe you generate even more sales.

With the increase in e-commerce, maybe where to locate is better optimized by solving for ease of delivery versus being in the heart of a trade area in a conspicuous location with an anchor nearby. Maybe the visibility they strive to optimize is social media visibility and not street presence.

Destination or Convenience?

I did site selection work for Home Depot and Canadian Tire about the same time.

A difference between the two was that Home Depot believed that potential customers went out of their way to find them. They are a destination that potential customers will find, and that complemented their philosophy for site selection. Canadian Tire thought they were a convenience retailer: potential customers went there because it was convenient for whatever they wanted to buy from them or their competitors.

That difference – destination or convenience – drove their preference for where to locate stores

E-commerce and Amazon Prime in particular disrupt this approach because now you do not even have to leave your home to do the shopping, and what you shopped for may arrive faster at your door that going out and getting it yourself. E-commerce is undermining Main Street retail for convenience.

U/X

Really? U/X from a machine? It is at best a subset of the full experience of dealing with someone of knowledge to guide a purchase. Particularly if you have an issue. Unfortunately bricks and mortar retailers are bridging the gap by making the in-store experience less rich and more e-commerce like.

My best comparison is that of seeing your favourite band live and up close versus way in the back at the big venue versus listening to them on a really good sound system versus listening to them on one of those little pod speakers with an MP3 file on the go. The experience is entirely different and much less rich.

Below is a store that exists in Trastevere in Rome. The discussion I had with the owner involved the folly of having 24-hour clocks for a planet that does not have 24-hour days. Where do all the 1/4 days go for three years before we have a leap year?

Polvere di Tempo, Trastevere Roma

{kind=link}

This store experience can’t be done on-line even with AR or VR. It can’t capture the smells and textures and reactions of the other customers experiencing delight in what the store sells. It will never replicate the experience I enjoyed and how its re-telling held sway at dinner parties for years. It is a tough store for social distancing.

Main Street Retail: doom, destruction and rebirth??

The most basic tenet for retail is potential sales and this is where Covid-19 may be the most insidious assault of all. My Main Street businesses are not responding to a competitive challenge or an economic challenge, but a public health situation that will takes years to normalize.

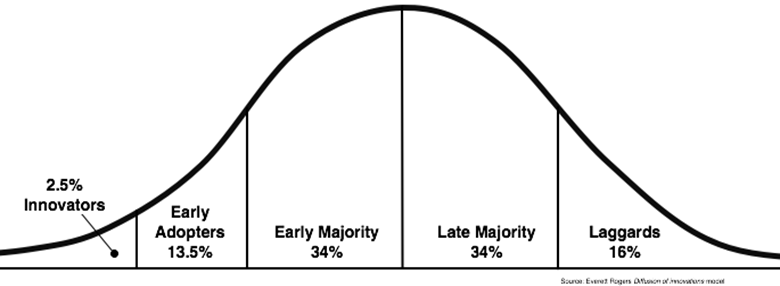

I am just not sure how long Covid-19 will affect the willingness of potential customers to make purchases from Main Street retail. I suspect that this recovery in sales will be governed by much the same adoption rate as is outlined in the diffusion of innovation.

{kind=link}

Likely the innovators and early adopters are already frequenting Main Street retail as Covid-19 protocols become more familiar and less bothersome. It will take a while before the 50% of the population that is late majority or laggards to get back frequenting these local establishments and get them back to pre-Covid-19 revenue.

With this fifth assault on Main Street retail, how will it turn out in your market?