We’re not perfect – we know that. We already have people to tell us that.

But if you would like to tell us about things we currently don’t do, or something that you would like to see from us, this is your chance.

Please leave a comment/suggestion/idea so we can improve our service offering, and help you make better decisions.

We’re not smart, handsome or clever, but we do learn from our mistakes, and try to improve every day.

why we suck

Here’s the thing. Our approach – it’s what we think is fundamental to ensuring our clients achieve their goals.

Firstly, we start with the end in mind. By that, we need to be aligned with where you want to get to, or understand your preferred outcome by making that acquisition or disposition. Once we have that goal in mind, we ensure our efforts are aimed at achieving that goal.

Secondly, real estate investing is an expectation for a future, not a recreation of a past. Where the market has been, or what has happened up until now is usually sufficient to know and rely upon in underwriting an investment, unless it isn’t.

Everything changes, market conditions change, tenant demands change, debt availability and terms change, and occasionally that change is not incremental but discontinuous. We are always on the hunt for hidden indicators that the market is about to change, and how that change may affect you. We are like army generals hoping to avoid fighting the last war again, and being focused on the battle that is looming.

Next, the real estate market is a collection of elements with differing life cycles. These include: the property life cycle;construction; steady state operations; capital investments; functional and physical obsolescence; redevelopment or demolition.

The leasing market life cycle: improving; peaking; declining; recovering.

The general economic cycle: expansion, peaking, recession/depression, recovery.

The debt market cycle: limited availability & poorer pricing; more availability & improving pricing; more availability & improving pricing & fewer covenant demands; reduced availability due to risk/reward imbalance & poorer pricing.

The other cycle is the investment criteria life cycle, or more properly evolution, for investors. Their interest in opportunity versus value-add versus core changes over their life and over the life of the other cycles in play. As well, the investments that are prudent and “core” change as the size of their portfolio changes, with the result that key holdings in the early stages are no longer key holdings later on.

Lastly, after years of dealing with many investors and sellers and owners, we find not everyone’s core holding is the same. Sometimes what is being sold is no longer in favour to the seller, but very much in favour to the buyer. Just because it is for sale does not mean it is broken or flawed or has an impending problem. It usually means that it just isn’t quite right for the existing owner, but it will be for the next owner.

We are in the business of finding that group that covets that property more. We optimize “covetedness”. That leads to liquidity, a more crowded trade and perhaps even seller pricing power.

hallmarks of our approach

We prefer to approach the underwriting process from the ground up. What is necessary to keep bums in seats? How does the building stack up against its top 3 competing buildings? How do the common areas and lobby stack up against the next tier up for quality?

We believe the competitive market for leasing opportunities is really the subset of buildings that most tenants find to be equivalent in terms of offering – location, amenities, price point.

We believe that the market vacancy statistics or the sub-market vacancy stats are not necessarily a good indicator for the demand/supply micro-climate for any one property. The important factor is which landlords are competing for this business, not necessarily how many options there are.

We believe that the principal point of the initial tour exercise is to get to a short list as quickly and as arbitrarily as possible. The first impressions for vacant space can happen a long time before the suite door is opened.

We look to confirm details from multiple and credible sources to ensure that the property is fully described with all the features and benefits that could accrue to the most likely qualified and motivated buyers. This is not the easy approach.

We believe that eventually buyers will find the problems and blemishes on the property for sale. We believe that it is better to describe them from the outset, provide a complementary context for the issues, and point to possible solutions.

We believe it is best to focus our efforts on selling to true believers, those who are in agreement with the investment thesis we provide to support the value expectations the seller has for its property. Those who are reticent about the property, or do not wholeheartedly accept the strengths of the property will not value it the highest.

We believe that if an outlier appears in a competitive bid date deadline, deal with the outlier. The herd gets mad finding out they were never in the game. And it is unlikely they will become the outlier in the next round.

We believe most tenants want to renew because it is painful to move. In most instances, the landlord chooses to have them stay, or becomes the principal driver for them choosing to relocate.

We believe that despite the drive to lease all the space in the building, it is important in the bigger buildings to have vacant space in order to to accommodate the best tenants in the building as they look to expand or contract or refurbish their premises.

We believe that the reporting on occupancy markets across North America does a disservice to a large part of the economy, and that part is all those tenants in buildings too small or different to be included in the “official stats”. In Ottawa, the “competitive” market for office space is quoted at 40 million SF and MPAC, the provincial tax assessment organization tracks 61 million SF for taxation purposes. Not a small discrepancy.

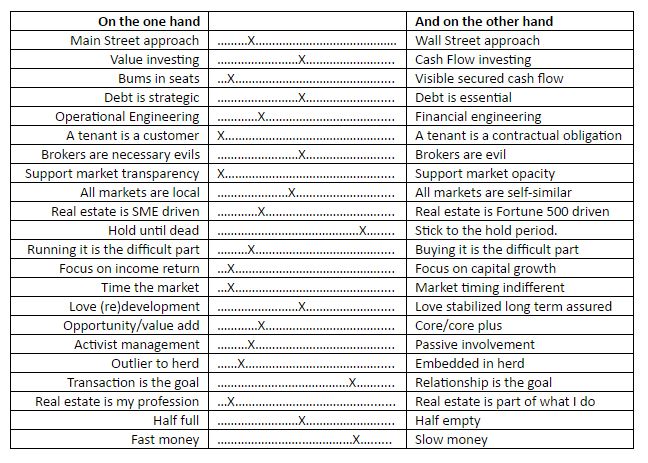

continuums

This is where we sit on continuums that help define investment style, and illustrate our approach to issues and problems. These differences point to what is sometimes more important to you, or how you find you usually act. There is nothing absolutely good or bad about any choice, however we may see the world fundamentally differently than you.

Please let us know how you feel about these issues, where we differ, and where we agree.

This website uses only recycled words